For further insights on investing in Angola, please email Managing Director Indigo Ellis on [email protected], or Associate Anna Westwell at [email protected].

On 24 August, Angolans will head to the polls for a general election. They will elect a parliament, and, by default, the country’s president – the leader of the party with the most votes. Incumbent president and leader of the Popular Movement for the Liberation of Angola (MPLA), João Lourenço, is seeking a second term in office.

As with other liberation parties in Southern Africa, popular support for the MPLA is falling. In the face of a stronger opposition, united for the first time against the MPLA, the stage is set for Angola’s most competitive election since the end of civil war in 2002. This insight unpacks the forthcoming election, highlighting the likeliest outcome – a Lourenço win, but with reduced vote share – and the most pressing issues voters will have in mind.

Lourenço win a sure bet, but reinvigorated opposition will gain

João Lourenço was elected in 2017 with the expectation that he would root out corruption and open the Angolan economy. However, Angolans have since grown dissatisfied, as despite Lourenço’s economic and political reforms, socio-economic conditions have not improved. GDP contracted for five consecutive years, from 2016 to 2020, and has only now begun to rebound marginally. There has also been little progress diversifying the oil-dependent economy, despite the president’s best efforts.

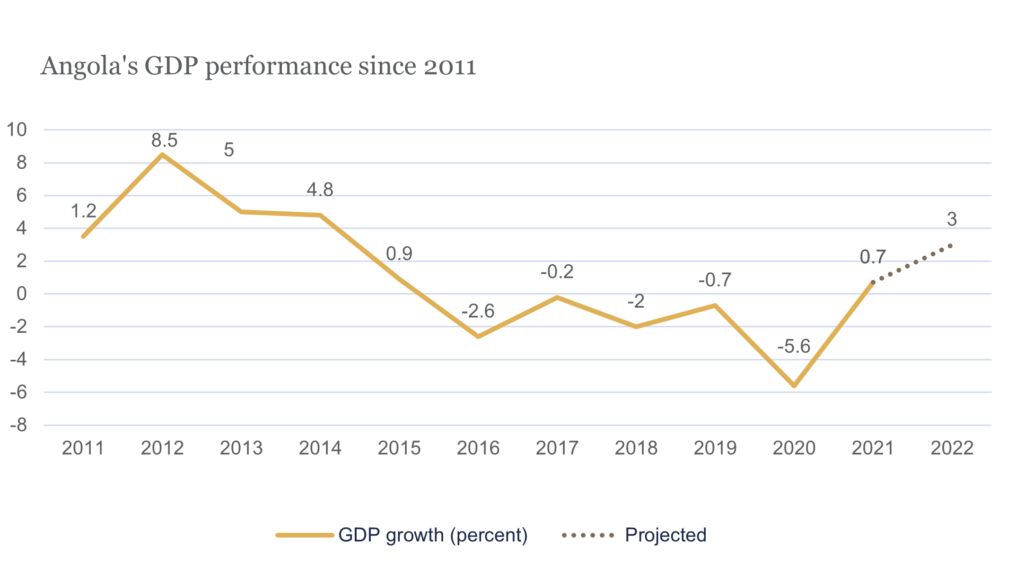

Source: IMF

Lourenço’s perceived inability to live up to his election promises means there is new hope for the opposition heading into August. In October 2021, Angola’s three main opposition parties formed a coalition to support a single presidential candidate to challenge the incumbent. The National Union for the Total Independence of Angola (UNITA), alongside the Angolan Renaissance Party – Together for Angola (PRA-JA Servir Angola) and the Democratic Block (BD), banded together to form the United Patriotic Front (FPU). Adalberto Costa Júnior – commonly known as ACJ – the UNITA president, has been chosen as the FPU candidate for the election.

The UNITA-led FPU is presenting a modern vision of Angola, threatening to claw away the urban youth vote from the MPLA. ACJ is a popular, charismatic leader. He represents a breakaway from the staid view of UNITA as a staunchly veteran-led, anti-foreigner party. ACJ is mixed-race and held Portuguese citizenship until 2019. He never fought in the Angolan civil war, having been posted as UNITA’s representative to Italy and the Vatican, where he became adept at fighting the party’s corner.

Amid this altered political landscape, there are four possible outcomes to the August poll. First, the MPLA could win again, but with a slimmer majority. Second, the MPLA could win a landslide victory, gaining a larger share of votes than they secured in 2017 (61 percent). Third, the newly formed coalition of opposition parties, the FPU, could win. Fourth, the result is a hung parliament – forcing the MPLA to curry support from one of the smaller FPU parties to secure a Lourenço second term.

The most likely result is yet another victory for the MPLA, but with a lower vote share. Voter repression tactics are likely, as is electoral fraud and obstruction, hindering the possibility of an outright opposition win, or even a hung parliament. The MPLA has a monopoly over state institutions and has an enormous financial advantage. UNITA has never held any meaningful level of power, and despite broadening its reach through a coalition, the party’s inexperience in government will be a disadvantage. ACJ is likely to win UNITA its largest vote share in decades, but he alone is unlikely to be enough to seize the presidential palace. A slim majority is unlikely to affect the policymaking process, nor alter Lourenço’s policy trajectory. In fact, continuity is likely.

Will businesses benefit from continuity?

An MPLA win is, broadly, good news for business in Angola. Victory will allow President Lourenço to continue his economic reform agenda and liberalisation drive, playing to the hearts of international investors. His priorities heading into a second term are continuing to privatise state assets and strengthening the democratic rule of law. Lourenço is also keenly focused on diversifying Angola’s resource exports, particularly in the mining and gas sectors. A win will give Lourenço the time needed to embed these changes, many of which have been in the offing for years.

A key test for his administration, and standing among international investors, will be the governance of August’s election. Anything short of internationally accepted – with minor interference – will threaten his reformist agenda, and his bid to improve the investment environment.

Anti-corruption and transparency will remain key priority

Despite his dwindling popularity over the course of his first term, Lourenço has differentiated himself from former president and autocratic ruler for 38 years, José Eduardo dos Santos. Dos Santos is in intensive care in Portugal, and while his potential passing is unlikely to affect the election outcome, it is likely to give Lourenço further political capital to continue his burgeoning anti-corruption drive.

This ongoing anti-graft campaign has targeted, albeit selectively, several members of dos Santos’ family, which has prompted widespread praise amongst the international community. Dos Santos senior’s passing would embolden Lourenço to chase further lost assets attributed to the dos Santos era. His transparency push has improved the ease of doing business in Angola and earned it a credit rating upgrade – achievements Lourenço is eager to bolster in his second term.

A notable success for Lourenço’s transparency drive in recent months has been Angola’s successful bid to join the Extractive Industry’s Transparency Initiative (EITI). Its membership will crystallise improved tendering processes and boost market attractiveness for new entrants in the oil and gas and mining sectors. President Lourenço has welcomed in companies keen to explore Angola’s mineral reserves outside of diamonds and iron ore – such as Anglo American, exploring for minerals crucial for the energy transition: copper, cobalt, and nickel.

New partners for Luanda as it turns away from China

Gaining new partners and reopening Angola to western investors will continue to be a key part of the president’s privatisation push after the election. Angola has seemingly turned away from China. Formerly, under dos Santos, Luanda enjoyed a close relationship with Beijing, however, Lourenço has distanced his regime from these former partners. In February 2020, for example, the government seized both of China International Fund’s – a subsidiary of controversial 88 Queensway Group – headquarters in Luanda.

Lourenço’s anti-China stance was well-evidenced this month, when he seized a stake in the Catoca diamond mine from ILI International, a subsidiary of China Sonangol, one of the most influential private Chinese investors in Angola. China Sonangol’s links to the previous dos Santos regime sealed its fate. Lourenço is adamant on creating new joint ventures to exploit Angola’s diamonds – potentially even at Catoca. But one complication is Russian state-owned company Alrosa’s involvement in the diamond sector, and at Catoca, where it has a stake. While it owns stakes in multiple mines, some of these sit below the 50 percent mark – above which US sanctions apply. Nevertheless, its involvement will spook western investors.

The government will also need to carefully navigate its search for new partners as it battles an ailing economy. Uprooting all of its Chinese contracts will be highly detrimental at a period of slow growth. As shown in the chart above, Angola’s GDP performance has suffered recently. A drop in oil production is to blame, but with rising crude prices, the kwanza is performing well – it strengthened 15 percent in 2021, buoyed by a tight monetary policy. Ailing production at its rival oil producer Nigeria meant that Angola was Africa’s largest oil producer in May 2022. And according to one of AML’s sources, an Angolan diplomat based in London, the government’s flagship privatisation programme has earned USD 1.8 billion from 73 asset privatisations since its 2018 launch.

While investors can expect more of the same priorities into a second Lourenço term, the seeds of change planted in his first term are beginning to sprout, giving AML cautious optimism.